Errors & Omissions (E&O) insurance, also known as professional liability insurance, is a type of liability insurance that protects your company from professional negligence lawsuits. Since these claims might take a long time to resolve, the financial impact on the company can be devastating.

Having the right small business insurance and E&O insurance policy for your agency is a necessity. Read on to learn more about what your company can gain from purchasing E&O insurance at Stampede Insurance.

Know More About E&O Insurance

Errors and omissions insurance often covers court expenses and settlements up to the amount specified in the insurance contract. This type of liability insurance is typically necessary for businesses that provide professional advice or services.

An organization could be held liable for millions of dollars in damages and the cost of hiring a legal team without E&O insurance. E&O insurance can assist in reducing or even eliminating these risks.

If an investment goes sideways, a client may sue an advisor or broker, even though the risks were well-known and within the client's bounds. Despite a court or arbitration panel ruling in favor of the broker or investment advisor, legal fees can be prohibitively costly, so E&O insurance is crucial to have when running a small business.

E&O Insurance Coverage

Protecting your small business from claims that can financially jeopardize your company's reputation is a troublesome situation without the right protection. Errors and omissions insurance safeguards your company against allegations of:

Negligence

Errors in the services provided

Omissions

Misrepresentation

Inaccurate information

In particular, it can help cover your attorney fees, court costs, administrative costs, and other settlements if someone sues your company for making a mistake in the professional services you've supplied.

Who Will Benefit From E&O Insurance?

Stampede Insurance's E&O coverage provides many benefits to businesses and people. Temporary employees, claims arising from work done before the policy was in effect, and claims in different jurisdictions may or may not be covered by E&O insurance.

Technology E&O insurance may be beneficial to the following types of technology professionals:

Producing electronic components for computers is a business.

Consultants in computer science

Providers of internet access

IT consultants

Developers of software

Developers of websites

Here are a few scenarios in which technology E&O insurance would be beneficial:

If a flaw in the software you offered caused a client's billing data to be ruined,

If the equipment you installed failed and a customer couldn't place orders,

If a website you built appears too much like a competitor's website, it's a red flag.

If you miss critical deadlines when developing a new technology product and lose money as a result,

If you sell a client the wrong product and their system crashes, it's your fault.

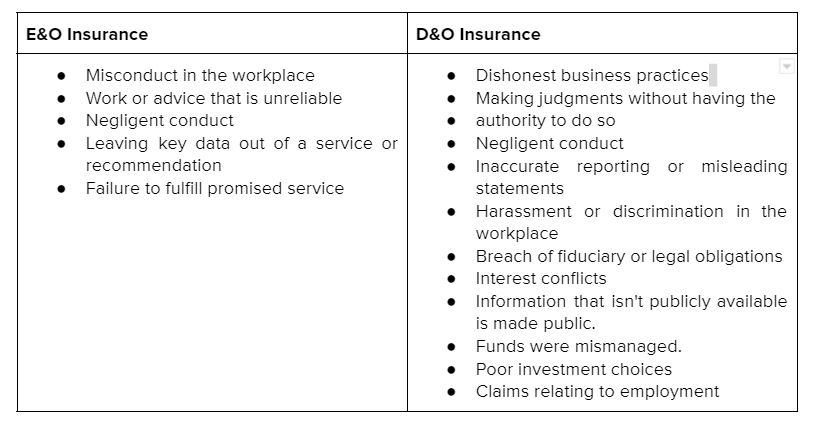

The sole difference between D&O and E&O insurance is the people who are covered financially. D&O insurance is designed to cover directors and officers who have been sued due to an error (or suspected error) they committed while operating a business.

Management liability insurance is another name for D&O insurance, while professional liability insurance, or malpractice insurance in the healthcare field, is another name for E&O insurance. Errors and omissions insurance protects firms that have made a mistake (or allegedly made a mistake) in a professional service or their advice, resulting in a financial loss to a third party.

Employees are the most common source of D&O claims, but they can also come from various other sources, including regulators, competitors, shareholders, and creditors. E&O claims, on the other hand, are typically brought by third parties, such as clients.

In addition, if you're proven not guilty in a criminal trial, D&O insurance can cover your defense costs. Employees, on the other hand, are not covered by E&O. E&O and D&O insurance covers the following types of situations:

Frequently Asked Questions

Find out more about E&O insurance by reading through these commonly asked questions by those interested in purchasing errors and omissions insurance.

What Is Errors and Omissions (E&O) Insurance and Why Do I Need It?

Professionals in financial areas such as insurance, investments, real estate, and accountancy will profit from E&O insurance because it will protect them in the case of a costly mistake or omission on behalf of a client. Many regulatory agencies require employees in these occupations to get E&O coverage, either through their company or independently.

What Are the Benefits of Errors and Omissions Insurance?

Suppose a client suffers a loss due to a mistake or omission made during the application, consultation, or investment decision. In that case, the client has the right to sue the financial expert. Legal fees and any damages payable to the client are covered by E&O insurance.

What is the distinction between general liability insurance and professional liability insurance?

Take every opportunity to make a smart choice by purchasing errors and omissions insurance for your small business or large enterprise. Professionals in financial industries will find this type of insurance a great investment for long-term business solutions.

Reach out to our professionals at Stampede Insurance to learn how you can explore how we can help elevate and scale your business with the right E&O insurance protection.

Located in Pasadena, California. We also serve the Anaheim, Long Beach, Los Angeles, Riverside, and San Bernardino areas. Licensed in Alabama, Arizona, California (#0H18184), Florida, Kansas, Kentucky, Louisiana, Mississippi, New Mexico, Nevada, Oklahoma and Texas